Shared ATM Networks: A Possible Direction for Banking Infrastructure

As banks continue to optimize costs and adapt to changing customer behavior, the structure of ATM networks is increasingly coming under review. One direction that continues to gain attention is the concept of shared ATM infrastructure – where multiple financial institutions rely on a common network rather than maintaining separate deployments.

While shared networks are not new, evolving market conditions and operational pressures are bringing renewed focus to this model.

Rethinking Traditional ATM Ownership

Historically, banks have managed their own ATM fleets, maintaining control over deployment, servicing, and customer experience. This approach offered flexibility but also required significant investment in hardware, operations, and ongoing maintenance.

In recent years, however, the economics of running large, independent ATM networks have become more challenging. Rising operational costs, combined with shifting transaction volumes in some regions, are prompting institutions to reconsider how these networks are structured.

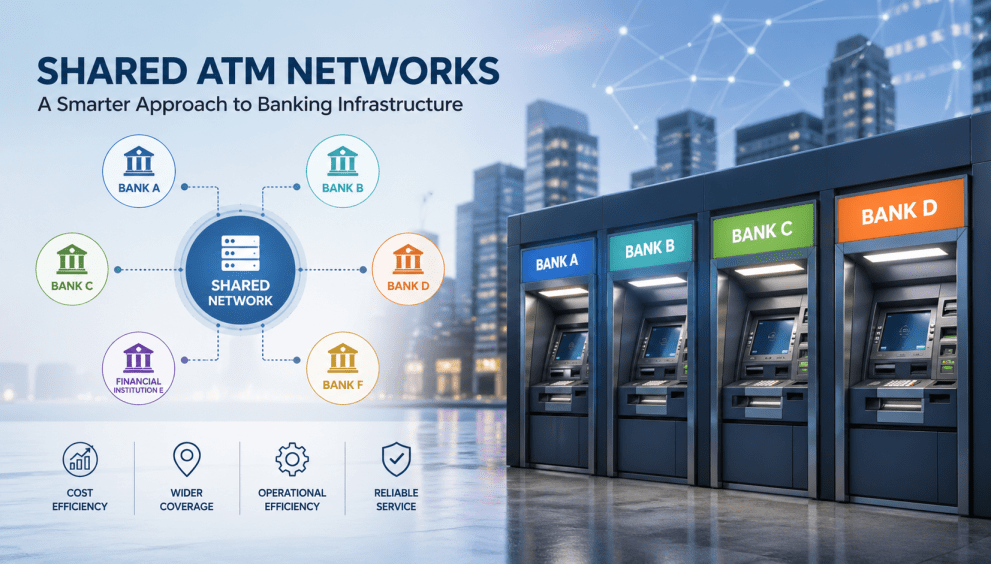

Shared infrastructure offers an alternative, where multiple banks can access a common network while focusing their resources on core services rather than physical infrastructure.

Operational Efficiency and Cost Considerations

One of the primary drivers behind shared ATM networks is efficiency. By consolidating infrastructure, organizations can reduce duplication across deployments, optimize geographic coverage, and share operational responsibilities.

This can translate into:

- lower capital expenditure for hardware deployment

- more efficient use of existing locations

- streamlined maintenance and service operations

For service providers, a shared model can also create opportunities to standardize processes and improve resource allocation across a larger, unified network.

Customer Experience in a Shared Environment

From a customer perspective, shared ATM networks can offer broader access to services without being limited to a specific bank’s footprint. In many markets, this approach already supports increased convenience, particularly in areas with fewer banking locations.

At the same time, maintaining a consistent user experience across shared infrastructure presents its own challenges. Branding, interface design, and service availability must be carefully managed to ensure that customers still recognize and trust the services they are using.

Balancing uniformity with institutional identity remains an important consideration in shared network models.

Technology and Integration Challenges

Transitioning toward shared ATM infrastructure requires careful coordination at both the technical and operational levels. Systems must support interoperability across different banking platforms, and integration with core systems becomes more complex when multiple institutions are involved.

Standardization plays a key role here, enabling different participants to operate within a common framework. At the same time, flexibility must be preserved to accommodate varying requirements across institutions.

These challenges are not purely technical – they also involve governance, security, and regulatory considerations that differ between markets.

Industry Context

Shared ATM networks are already established in some regions, often supported by independent operators or consortium-based models. As financial institutions continue to look for ways to optimize operations, these models are gaining renewed attention.

In parallel, the broader shift toward platform-based services in banking is reinforcing the idea that infrastructure can be shared, while differentiation moves to the service layer.

The move toward shared ATM infrastructure reflects a broader trend in the industry: separating physical infrastructure from service delivery.

For banks, this can mean greater focus on digital services and customer engagement, while relying on shared networks to maintain access to cash and essential self-service functions.

At the same time, the success of such models depends on execution—particularly in areas such as reliability, service quality, and coordination between participating organizations.

Conclusion

Shared ATM networks are not a new concept, but changing market dynamics are making them increasingly relevant. As institutions seek to balance cost, coverage, and service quality, shared infrastructure models may play a larger role in shaping the future of ATM deployments.

While the path forward will vary by region and regulatory environment, the underlying question remains consistent: how to deliver reliable, accessible services while managing the complexity and cost of physical networks.